Renewables in Italy: Opportunities for International Investors

Italy remains a compelling market for renewable energy investment. Strong power demand, a mature regulatory framework and attractive resource conditions – particularly for solar and selected wind areas – make it well suited for both single-asset acquisitions and portfolio strategies. In this context, setting up an Italian special purpose vehicle (SPV) is often a practical tool to acquire and operate renewable assets, ring-fence project risks and streamline financing and M&A execution. In this article, Ecovis consultants, together with Erica Alessandra Westmore, an independent advisor supporting SPV representation in Italy and M&A transactions involving photovoltaic assets, outline why Italy is attractive, which SPV formats are commonly used, the practical set-up and the tax and digital-compliance points international sponsors should factor into their timelines.

Overview

Why Italy is attractive for renewable investments

Italy remains an attractive destination for renewable energy investment, supported by a policy framework that continues to encourage new capacity and a permitting system that, for eligible plants and depending on location, may offer streamlined authorization pathways.

Backed by strong demand drivers and favorable solar and wind conditions, Italy also benefits from a well-developed ecosystem of lenders, technical advisors and contractors – an important factor for executing transactions efficiently and scaling multi-asset platforms.

Why use an Italian SPV (and when you need more than one)

Using an Italian SPV is usually the preferred route for acquiring and managing renewable energy assets because it allows access to the Italian market and to local assets while reducing the risk at the parent-company level, as liabilities are ring-fenced within the project company. It also enables investors to separate each “parcel” of assets, making acquisition and sale of projects easier and facilitating the separate financing of each investment.

As a practical rule, investors often adopt:

- one platform company (holding/coordination) and

- one SPV per project (or per financing perimeter).

Compliance note for non-Italian investors: while there are generally no “blanket” prohibitions on foreign participation, the deal timeline should include a check on any reciprocity-related notarial requirements and, where relevant, Golden Power notifications for strategic sectors.

Which company types are commonly used

The most common form for an SPV is the SRL (Società a Responsabilità Limitata), the Italian equivalent of a limited liability company. Shareholders’ liability is limited to the capital they have subscribed, the minimum share capital is EUR 10,000, and governance can be entrusted either to a sole director or to a board of directors; the SRL can be single-member or have multiple shareholders.

Another frequently used vehicle is the SAS (Società in Accomandita Semplice), a limited partnership with mixed liability. It has two categories of partners: general partners (soci accomandatari), who are personally liable with all their assets, and limited partners (soci accomandanti), who are liable only up to their contributions; the general partner may itself be an SRL, allowing investors to limit personal exposure. The SAS has no mandatory minimum share capital and benefits from simplified accounting and corporate formalities.

Key incorporation and onboarding steps

Setting up an Italian SPV typically involves a sequence of pre-incorporation, incorporation and post-incorporation steps.

Pre-incorporation steps: shareholders and directors obtain an Italian tax identification number (codice fiscale), complete the KYC/AML documentation required by the notary and the bank and open a bank account to fund the share capital.

Incorporation steps: the company is then incorporated before an Italian notary, who formalizes the incorporation deed and by-laws, verifies corporate powers and registers the legal address, followed by filing with the Register of Companies and activation of a PEC (certified email) for official communications.

Post-incorporation steps: finally, the SPV completes the operational onboarding, including VAT registration, set-up of accounting and VAT processes, maintenance of mandatory corporate/accounting books (for SRLs), and any commencement/operational notices with the competent authorities depending on the planned activity.

Where foreign parties must sign deeds or complete filings, it is advisable to align powers of attorney and any apostille/legalization requirements early, as these formalities often become the main driver of the timetable; in parallel, the governance documentation should be drafted to reflect the intended governance model and any project finance requirements (e.g., signing powers, reserved matters and lender covenants), and the SPV should be organized for ongoing compliance: appointment of an accountant/tax adviser, bookkeeping, VAT, annual financial statements and corporate income tax filings – together with any employment/payroll arrangements and ancillary contracts (such as leases, intra-group loans and service agreements), in line with applicable AML/KYC obligations.

Key tax aspects

Italian SPVs are subject to corporate income tax (IRES) at a standard rate of 24% and to regional tax on productive activities (IRAP), generally around 3.9%, with possible variations depending on the region of the registered office. Property tax (IMU) applies on the basis of the cadastral classification of the assets and the rates set by each municipality where the assets are located.

Dividends distributed by Italian companies to non-resident corporate shareholders are, as a rule, subject to a 26% withholding tax. This rate may, however, be reduced or eliminated by applying the EU Parent-Subsidiary Directive or the relevant double tax treaties, which cover all EU countries and many other jurisdictions worldwide.

Digital “e-bureaucracy” in practice

Italy has progressively digitized corporate and tax compliance. In day-to-day operations, investors will encounter:

- Certified Email (PEC) as the default channel for many formal communications, with legal equivalence to registered mail;

- Digital Signatures are standard, and Electronic Invoices are mandatory, ensuring full transparency and automatic accounting updates;

- increasing use of Digital Identity and remote identification procedures depending on the role and residency status of directors / signatories;

- Court and Administrative Procedures increasingly rely on online platforms. For civil court proceedings, documentation is filed digitally, notifications are sent electronically and hearings may be held online, allowing foreign investors and their advisers to manage many steps remotely.

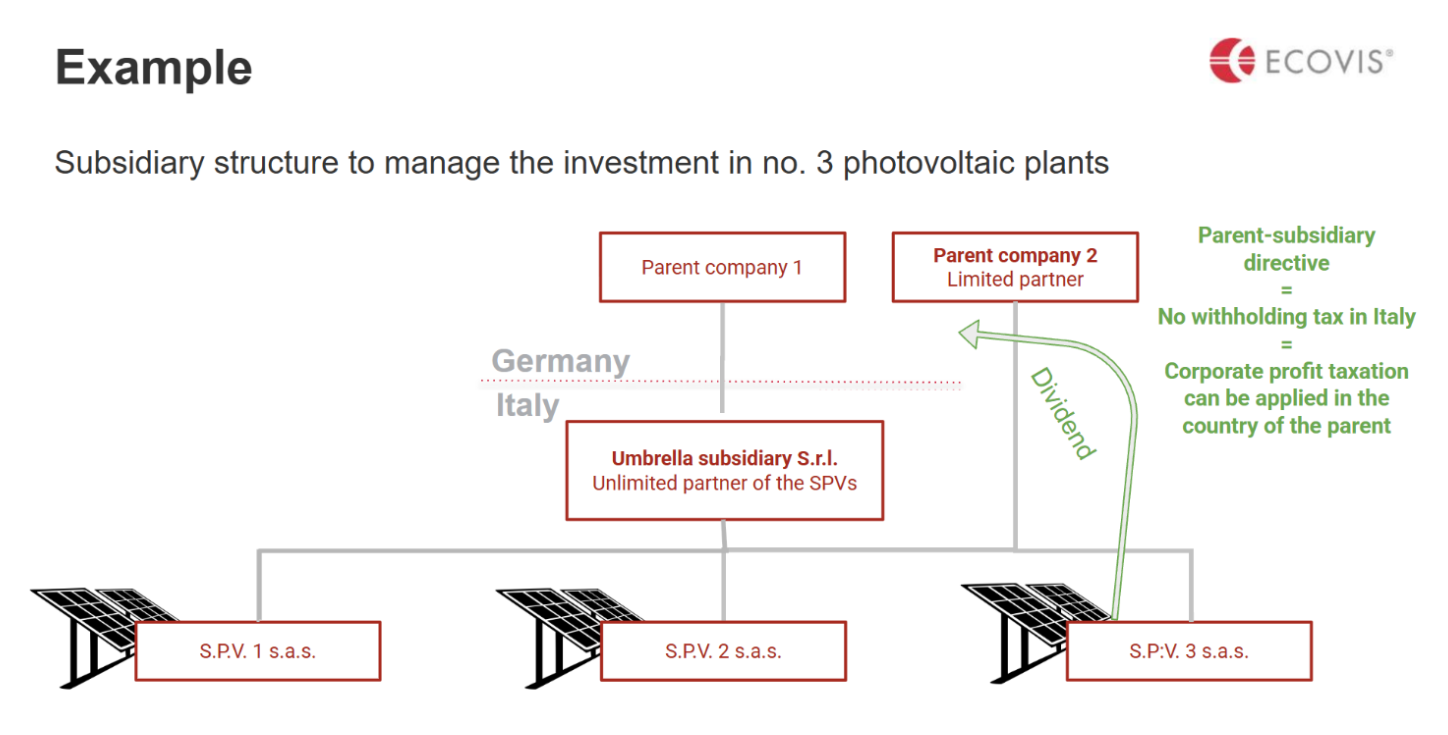

Example structure: more photovoltaic plants under a single platform

A typical structure for three photovoltaic plants involves an Italian umbrella subsidiary in the form of an SRL, owned by a foreign parent company. This umbrella SRL acts as unlimited partner in several Italian limited partnerships (SAS), each of which holds a single photovoltaic project, while the foreign parent remains a limited partner. Dividends flow from the SPVs to the parent company, and, where the conditions of the Parent-Subsidiary Directive are met, no withholding tax is levied in Italy, so corporate profits can be taxed in the country of the parent.

This approach helps lenders and buyers assess each project on a standalone basis, while preserving central control and reporting at platform level.